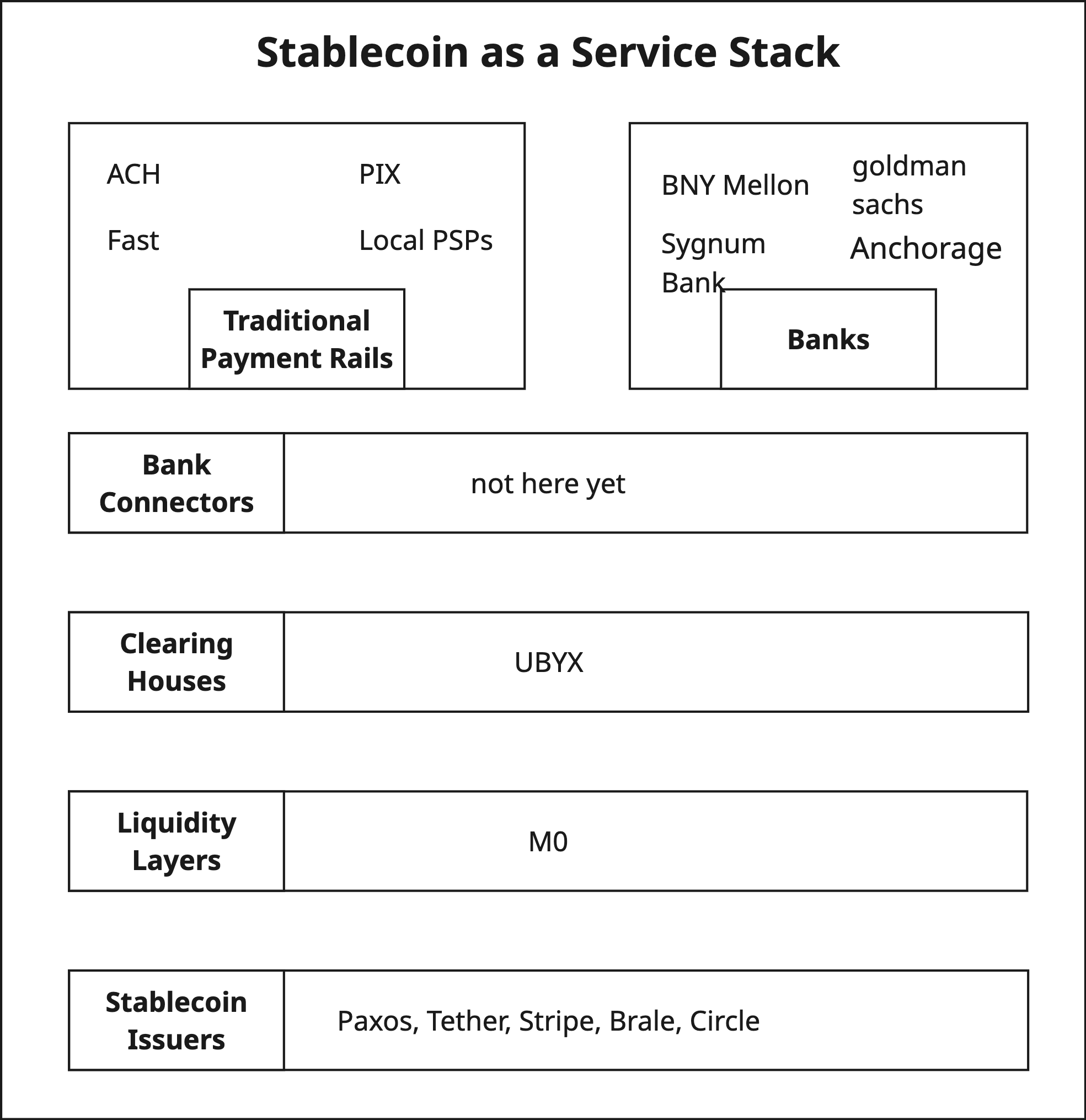

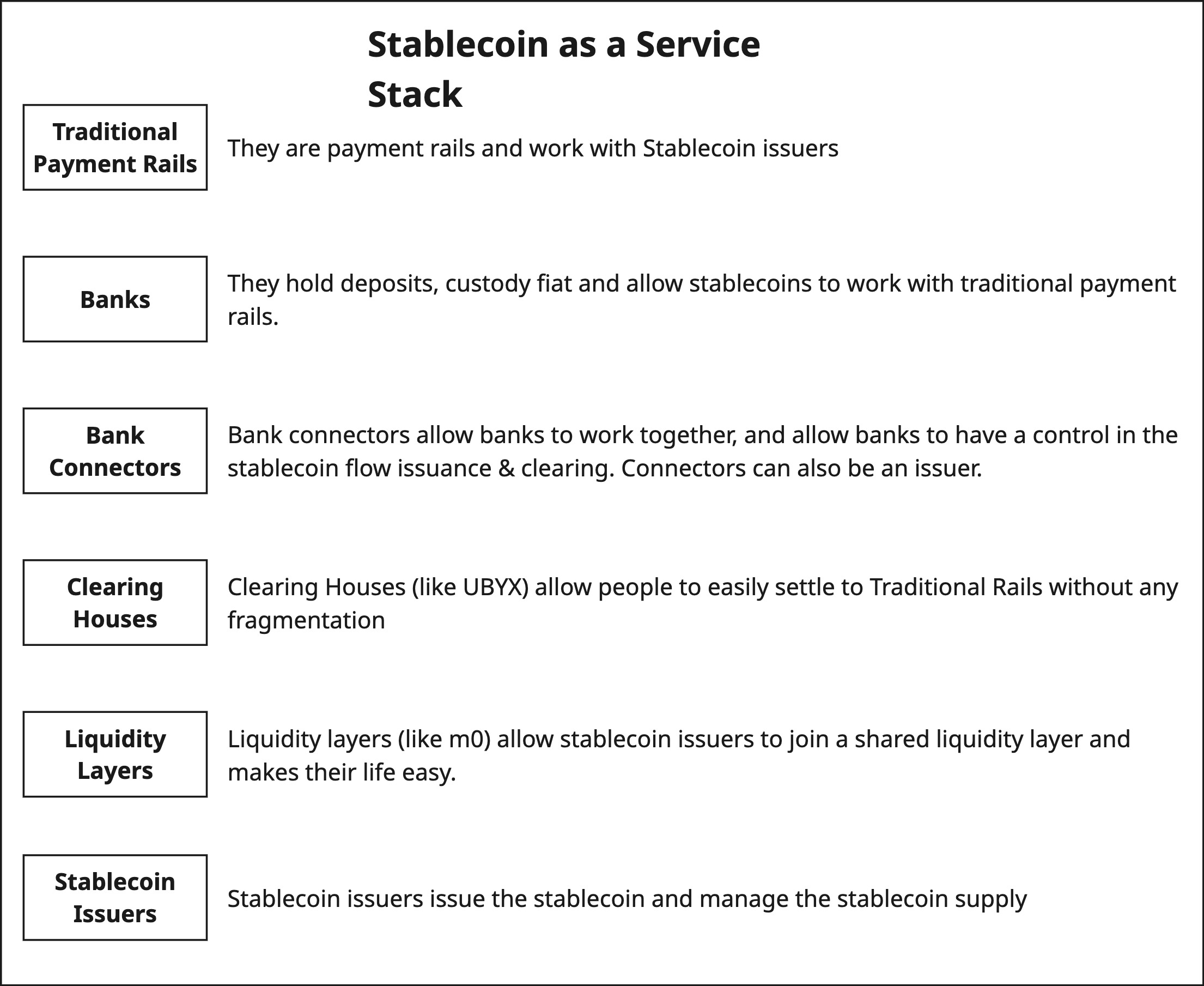

Stablecoin as a Service Stack

Stablecoins are becoming modular, and there are new parts that have emerged in the stack. In this article I explain the parts and what they do.

We shared our thesis about stablecoin issuance five months ago, which we called “Visa for Stablecoins.” The market is rapidly changing and validating that thesis. For example:

M0 has grown its TVS (Total Value Secured) by 300%.

Stripe announced its open issuance platform and standard.

UBYX completed its first clearing transaction.

The market is clearly evolving, and the “Stablecoin as a Service” stack is rapidly expanding with it. In this blog post, I want to explain this stack and why it’s growing.

1.1. Stablecoin Issuers

After the Genius Act was passed, the path to stablecoin issuance became much clearer. Almost any financial institution that holds the necessary licenses and follows capital requirements can now be an issuer. We now see Bridge (Stripe’s company), Paxos, Circle, Brale, and MXON (M0’s stablecoin issuer company) in the space. There is a lot of competition, and as the market becomes more competitive, profit margins are reducing every day.

1.2. Liquidity Layers

As the stablecoin issuance market becomes more competitive, a new need has emerged. All new stablecoins face a “cold start” problem and need a liquidity network to solve it. This is why these new liquidity layers have appeared. They work with stablecoin issuers to allow for the creation of a joint liquidity network.

1.3. Clearing Houses

With so many new stablecoins coming to market, it becomes very difficult for users and businesses to handle them all. This creates a significant need for a clearing layer. This is why platforms like UBYX are important: they allow different stablecoins to connect with traditional rails while maintaining their individual sovereignty.

1.4. Bank Connectors

It is clear that banks will play a crucial role in the stablecoin stack, but they currently lack a standardized way to interoperate. They need a neutral network that allows them to share liquidity, especially during a massive liquidity event (as happened to Circle in the past, and will likely happen again). Bank networks like A+ allow banks to join a common network to issue, freeze, and manage issuance on bank deposits (assuming the network is designed with the right incentives). There is no “public” company building this, but it is coming :)

1.5. Banks

Banks are critical to finance: they manage liquidity, connect to payment rails, serve retail clients, and so on. They aren’t going anywhere. In fact, they are becoming even bigger stakeholders in the stablecoin ecosystem.

1.6. Traditional Rails

The crypto market has very little liquidity compared to what runs on traditional rails. This is why traditional rails are a crucial part of the stablecoin stack and aren’t going anywhere. There will always be a need for ACH, Fast, and other payment rails to ensure smooth rebalancing for market makers and large institutions.

2.1. The Future Ahead

We have seen issuers like Paxos and Circle hold a great moat in the stablecoin market, but after the Genius Act, that’s changed. The stack is becoming modular, and all the different services stablecoins provide are becoming new markets. Liquidity is one, and bank connectivity is another. We will see more and more projects come into this market.

I believe the market will continue to take shape. Gaps will appear, and those gaps will create new submarkets within the stablecoin business. There will be new winners in each submarket. If you’re building something in this space, feel free to DM me on X!